Uber and Lyft Accidents in Southern California: What the 2026 SB 371 Insurance Changes Mean for Injured Victims

Millions of Southern Californians climb into Uber and Lyft vehicles every single day — heading to work in downtown Los Angeles, catching rides home from Gaslamp in San Diego, or getting picked up after a night out in Long Beach. Ridesharing has become as routine as driving, but many passengers have no idea that a major legal change took effect on January 1, 2026 that could significantly reduce the compensation they receive if a crash leaves them injured.

California's Senate Bill 371 (SB 371) quietly reshaped the insurance landscape for rideshare accident victims, slashing the uninsured and underinsured motorist (UM/UIM) coverage that passengers can access through Uber and Lyft. If you or a loved one has been hurt in a rideshare accident in Southern California, understanding this new law — and what protections remain — could be the difference between a fair recovery and a devastating financial shortfall.

What Is SB 371 and How Does It Affect Rideshare Accident Victims in California?

Senate Bill 371, signed into law during the 2025 California legislative session and effective as of January 1, 2026, made a critical change to the insurance requirements for Transportation Network Companies (TNCs) like Uber and Lyft. Specifically, it drastically reduced the mandatory uninsured/underinsured motorist (UM/UIM) coverage these companies must carry for passengers.

Before this law took effect, Uber and Lyft were required to maintain $1 million in UM/UIM coverage per incident — a substantial safety net that ensured passengers were protected even if the other driver in a crash was uninsured or underinsured. Under SB 371, that figure was cut to:

- $60,000 per person

- $300,000 per incident

That represents a reduction of roughly 94% in per-person coverage. In a region like Southern California — where a single emergency room visit, CT scan, and short hospital stay can easily exceed $50,000 — this change leaves many seriously injured passengers with coverage that runs out long before their medical needs are met.

It is critical to understand what SB 371 did not change. The $1 million third-party liability policy that applies when the rideshare driver is at fault for the accident remains fully intact. The coverage reduction targets only the UM/UIM component — situations where a third-party driver with little or no insurance causes the crash. In highly congested Southern California, where nearly one in six drivers operates without adequate insurance, that is an enormous gap.

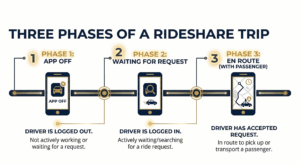

The three insurance periods in a California rideshare trip determine who pays after a crash under 2026 law.

Understanding the Three Insurance Periods in a California Rideshare Trip

One of the most confusing aspects of any Uber or Lyft accident claim is determining which insurance policy actually applies. California law, governed in part by California Public Utilities Code § 5433, divides each rideshare trip into distinct phases. Coverage depends entirely on which phase the driver was in at the moment of the crash:

- Period 1 – App Off: The driver's rideshare app is completely offline. In this situation, only the driver's personal auto insurance applies. Rideshare companies carry no coverage at all. If that personal policy has low limits or excludes commercial use, you may have very limited recourse.

- Period 2 – App On, Waiting for a Ride Request: The driver is logged into the app but has not yet accepted a fare. Uber and Lyft provide contingent liability coverage at limited levels — typically $50,000 per person / $100,000 per accident for bodily injury, plus $25,000 for property damage — only if the driver's personal insurance does not apply.

- Period 3 – En Route to Pickup or Transporting a Passenger: This is the phase most people associate with a “rideshare ride.” When the driver has accepted a trip and is either heading to pick you up or actively carrying you, the full $1 million third-party liability policy from Uber or Lyft activates. However, under SB 371, UM/UIM coverage is now capped at $60,000 per person if the at-fault party is a third driver.

Establishing exactly which period applies requires a careful review of app data, GPS records, and police reports — evidence your attorney should gather immediately after an accident.

Why Did California Pass SB 371? The Controversy Behind the Law

SB 371 did not pass without opposition. The bill became a flashpoint between consumer advocates and rideshare giants, with Uber and Lyft lobbying heavily for the change. Their stated argument was that the $1 million UM/UIM requirement was far more than what is mandated for any other commercial vehicle on California roads, and that the inflated costs were being passed on to riders through higher fares.

Critics, including the Consumer Attorneys of California (CAOC), pushed back forcefully. They argued that the legislation effectively transfers financial risk away from billion-dollar corporations and onto the injured passengers least able to absorb it. The coverage reduction was also paired with a separate legislative deal: Assembly Bill 1340, which gave rideshare drivers the right to unionize and engage in collective bargaining — a historic first for gig workers in California.

What Compensation Can You Still Recover After a Rideshare Accident in Southern California?

Despite the SB 371 changes, injured passengers, pedestrians, and other motorists still have meaningful legal options. The key is understanding which avenues of recovery remain open.

If the rideshare driver caused the accident, the $1 million liability policy is still fully available during Period 3. This covers:

- Medical expenses — emergency care, surgery, rehabilitation, future medical treatment

- Lost wages and loss of earning capacity

- Pain and suffering — California does not cap non-economic damages in standard personal injury cases

- Property damage

- Wrongful death damages for surviving family members

If a third-party uninsured driver caused the crash, recovery becomes more complex under SB 371. However, injured passengers may still access additional compensation through:

- Your own personal auto insurance UM/UIM policy — if you own a vehicle, your own policy can typically step in to cover you as a passenger in someone else's vehicle, including an Uber or Lyft. Reviewing your own coverage limits before you need them is wise.

- Direct claims against the at-fault driver personally, including their assets

- Claims against third parties — a defective road, a negligent vehicle manufacturer, or a negligent employer of another driver

- Health insurance for immediate medical coverage while the legal claim is pending

An experienced Southern California rideshare accident attorney will analyze every available layer of coverage to build the strongest possible recovery strategy for your specific situation.

Consulting a Southern California rideshare accident attorney after an Uber or Lyft crash can protect your right to full compensation.

How to Protect Yourself After an Uber or Lyft Accident in Southern California

The moments and days following a rideshare accident are critical. What you do — and what you avoid doing — can significantly affect the value of your claim. Follow these steps carefully:

- Call 911 immediately. Even if injuries seem minor, request police and emergency medical services. A formal police report is foundational to any personal injury claim. Do not rely on Uber or Lyft's in-app reporting as a substitute for an official law enforcement report.

- Seek medical attention without delay. Common rideshare crash injuries — including whiplash, traumatic brain injuries, and soft tissue damage — may not produce obvious symptoms for hours or days. A documented medical evaluation creates the evidentiary link between the accident and your injuries, which insurance companies will otherwise challenge.

- Document the scene thoroughly. Photograph all vehicle damage, road conditions, traffic signs, skid marks, and your visible injuries. Screenshot the trip details from your Uber or Lyft app, including the driver's name, vehicle information, and the precise time and GPS route of your ride.

- Collect witness information. Names and phone numbers of bystanders who saw the crash can be invaluable when liability is disputed.

- Do not give recorded statements to any insurance adjuster — not the rideshare company's insurer, not the other driver's insurer, and potentially not even your own — before consulting with an attorney. Early statements are routinely used to minimize or deny claims.

- Report the accident in the app. Use the Uber or Lyft safety reporting function within the app to create a formal record with the rideshare company, in addition to your police report.

- Consult a rideshare accident attorney promptly. Under California Code of Civil Procedure § 335.1, you generally have two years from the date of the accident to file a personal injury lawsuit. Acting early preserves evidence, secures witness memories, and gives your legal team the most options.

The Role of Proposition 22 in California Rideshare Accident Claims

Any discussion of Uber and Lyft liability in California must account for Proposition 22, the 2020 ballot initiative that classified rideshare and delivery drivers as independent contractors rather than employees. This distinction carries enormous practical consequences for injured victims.

Because Uber and Lyft drivers are not legally classified as employees, the companies generally cannot be held vicariously liable for driver negligence under the traditional employer-employee doctrine. Instead, injured parties typically pursue claims through the rideshare company's insurance policies rather than directly against the corporation itself as an employer. This framework shifts the focus to whether the required insurance coverage applies — and with SB 371's reductions in UM/UIM limits, that coverage is now thinner than at any point in recent California history.

However, direct corporate liability against Uber or Lyft may still be available in narrower circumstances, such as when the company was negligent in its driver screening, background check processes, or vehicle maintenance requirements. Courts have continued to scrutinize these companies' accountability obligations even under Prop 22's constraints.

Rideshare vehicle drop-offs in crosswalks and bike lanes create serious injury risks for pedestrians and cyclists in Southern California.

Special Concerns: Pedestrians, Cyclists, and Other Drivers Struck by Rideshare Vehicles

Rideshare accident claims are not limited to passengers. Southern California's dense urban environment means that Uber and Lyft vehicles frequently interact with cyclists, pedestrians, and motorists in complex traffic scenarios. Drop-offs in bike lanes, pickups at crosswalks, and sudden stops on congested streets like Wilshire Boulevard, Sunset Boulevard, and Pacific Coast Highway create constant hazard zones for non-passengers.

If you were struck by an Uber or Lyft vehicle as a pedestrian, cyclist, or occupant of another vehicle and the rideshare driver was at fault during Period 3, you are potentially entitled to claim against the full $1 million third-party liability policy. The SB 371 reductions in UM/UIM coverage do not affect this pathway — they only affect the separate situation where a different, uninsured driver is at fault and you are seeking coverage through the rideshare company's UM/UIM policy.

Pedestrian and bicycle accident victims in these cases often sustain some of the most catastrophic injuries: broken bones, spinal cord injuries, traumatic brain injuries, and in the worst cases, fatal outcomes. California law does not cap non-economic damages in these cases, meaning a skilled attorney can pursue full compensation for pain, suffering, and the long-term impact on your quality of life.

How SB 371 Changes Your Settlement Strategy: What Attorneys Are Doing Differently in 2026

Experienced Southern California personal injury attorneys have already adjusted their approach to rideshare accident cases in light of SB 371. If you are evaluating legal representation for a rideshare injury claim, ask whether your attorney is taking the following steps:

- Reviewing your personal auto insurance policy at the outset of every rideshare case to determine whether your own UM/UIM coverage can supplement the reduced rideshare company limits

- Pursuing all available defendants — including the at-fault third-party driver and any other potentially liable parties — to maximize recovery beyond the UM/UIM caps

- Preserving app data and GPS records immediately, before they are overwritten or become unavailable, to nail down which insurance period applies

- Building comprehensive damages packages that fully document future medical costs, lost earning capacity, and non-economic losses — ensuring that any available policy limits are fully justified

- Monitoring the November 2026 ballot initiative and advising clients on timing considerations that may affect the resolution of active claims

Key Facts About Rideshare Accident Claims and SB 371 in Southern California

Here is a condensed reference guide for accident victims and their families navigating the post-SB 371 landscape:

- Effective date of SB 371: January 1, 2026

- UM/UIM coverage before SB 371: $1,000,000 per incident

- UM/UIM coverage after SB 371: $60,000 per person / $300,000 per incident

- Third-party liability during Period 3: Still $1,000,000 — unchanged by SB 371

- Coverage during Period 2 (app on, no ride accepted): $50,000 per person / $100,000 per accident bodily injury

- Driver classification: Independent contractor under Proposition 22

- Statute of limitations: 2 years from the accident date under CCP § 335.1

- Best step after a crash: Contact a Southern California rideshare accident attorney before speaking to any insurance adjuster

- Governing authority: California Public Utilities Commission (CPUC)

How SB 371 Changed Coverage for Rideshare Accidents in SoCal

Injured in an Uber or Lyft Accident in Southern California? Napolin Accident Injury Lawyer Is Here to Fight for You.

The insurance changes brought by SB 371 make it more important than ever to have an experienced, aggressive advocate on your side from the moment an accident occurs. At Napolin Accident Injury Lawyer, we have built our practice in the heart of Southern California fighting for the rights of people who have been hurt through no fault of their own — including riders, passengers, pedestrians, and motorists impacted by rideshare accidents.

Our firm understands the complex, multi-layered insurance structure that governs Uber and Lyft accident claims, and we know how to navigate the changes SB 371 introduced in 2026. We take a deeply personalized approach to every case, taking the time to understand your injuries, your losses, and your goals before building a strategy tailored to your needs. We are committed to pursuing the maximum compensation available under California law — not the first lowball offer an insurance adjuster puts on the table.

Our track record of successful results in Southern California personal injury cases speaks for itself. When you work with Napolin Accident Injury Lawyer, you are not a case number — you are a person whose recovery matters to us.

Call us today at (866)-NAPOLIN for a free, no-obligation consultation. We handle rideshare accident cases on a contingency fee basis — you pay nothing unless we win for you. Do not wait: the evidence you need starts disappearing the moment the crash happens.

- Uber and Lyft Accidents in Southern California: What the 2026 SB 371 Insurance Changes Mean for Injured Victims - March 9, 2026

- Understanding Auto Accidents in the Rain: Key Causes and Risks for Southern California Drivers - December 23, 2025

- Understanding Hit-and-Run Accidents That Cause Crush Injuries in California - December 14, 2025